Namibia Offshore Exploration and Lessons for Pakistan

Namibia’s offshore exploration history offers a remarkable case study for nations like Pakistan aiming to unlock their hydrocarbon potential. Both countries have faced challenges in establishing offshore oil and gas production despite promising geological settings. By examining Namibia’s approach and outcomes, Pakistan can identify actionable strategies to rejuvenate its offshore exploration efforts.

Namibia’s Offshore Exploration Journey: Key Phases and Insights

- Early Licensing Rounds (1969–1979)

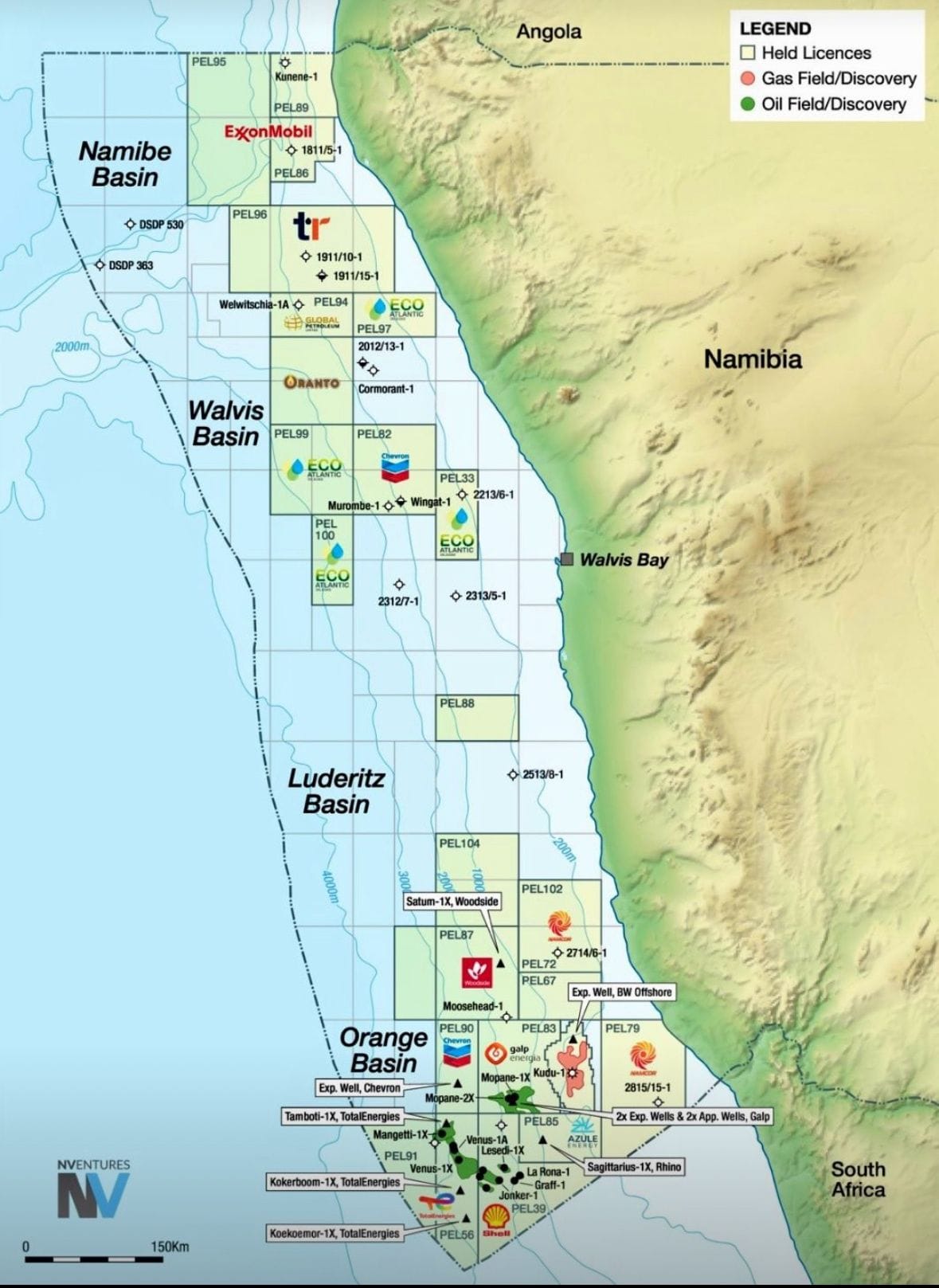

Namibia initiated its offshore exploration in 1969, awarding eight blocks during the first licensing round. The Kudu Gas discovery (Kudu 9A-1) by Chevron, Regent, and SOEKOR marked the first gas find in the Orange Basin. However, UN sanctions in the late 1970s halted international participation, with rights transferred to the nascent national oil company, SWAKOR.

2. Renewed Exploration Efforts (1987–1990)

With collaboration from Halliburton, SWAKOR conducted seismic surveys and drilled additional wells (Kudu 9A-2 and 9A-3). Despite limited success, the groundwork was laid for modern exploration techniques and resource assessment.

- Post-Independence Licensing Rounds (1990s)

- Namibia launched a series of licensing rounds from 1991 to 1999, awarding blocks to international players like Shell, Chevron, and Sasol.

- Exploration activity surged with over 88,000 km of 2D seismic data collected and multiple exploratory wells drilled. While discoveries were elusive, critical insights into basin geology were gained.

- Open Licensing System and Modern Discoveries (1999–Present)

The adoption of an open licensing system in 1999 attracted numerous global operators, including Shell and TotalEnergies. Key outcomes included:

- Enhanced seismic data acquisition with advanced 2D and 3D surveys.

- Significant light oil discoveries in 2021/2022 by Shell Namibia (Graff-1) and TotalEnergies (Venus-1X.T1) in the Orange Basin.

Figure courtesy to NVENTURES.

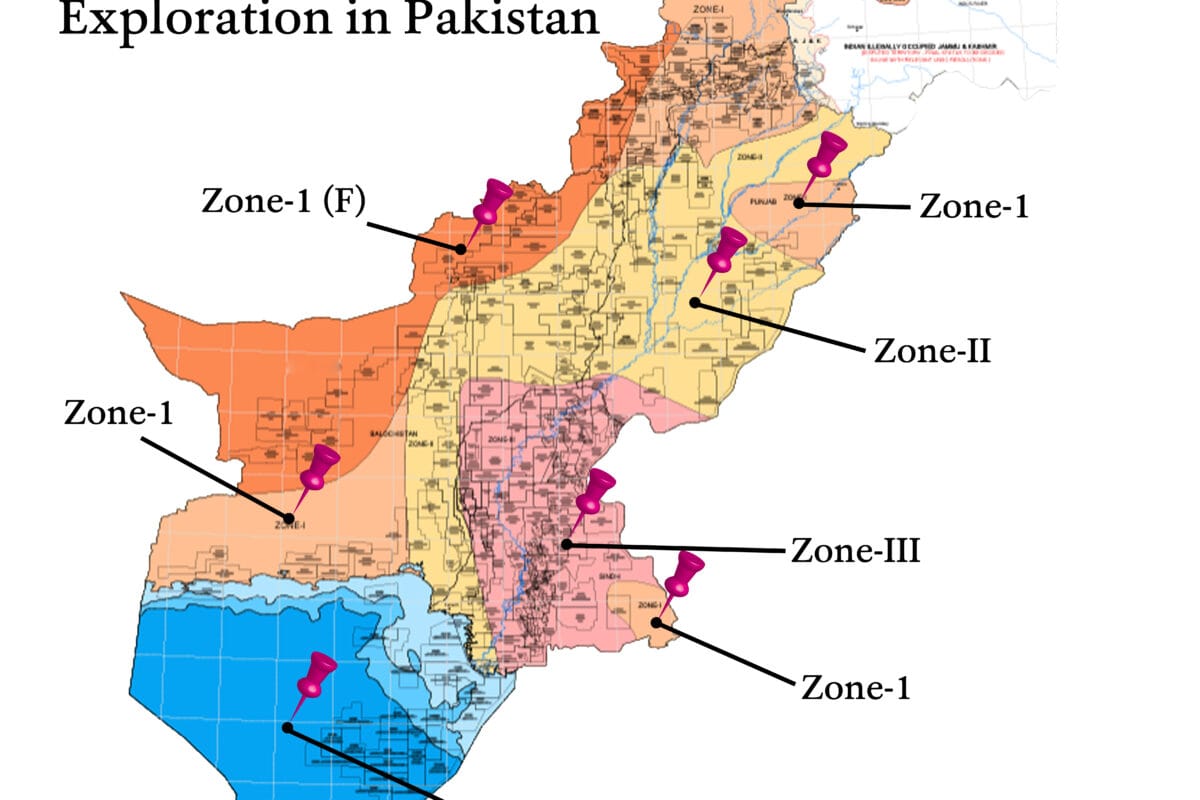

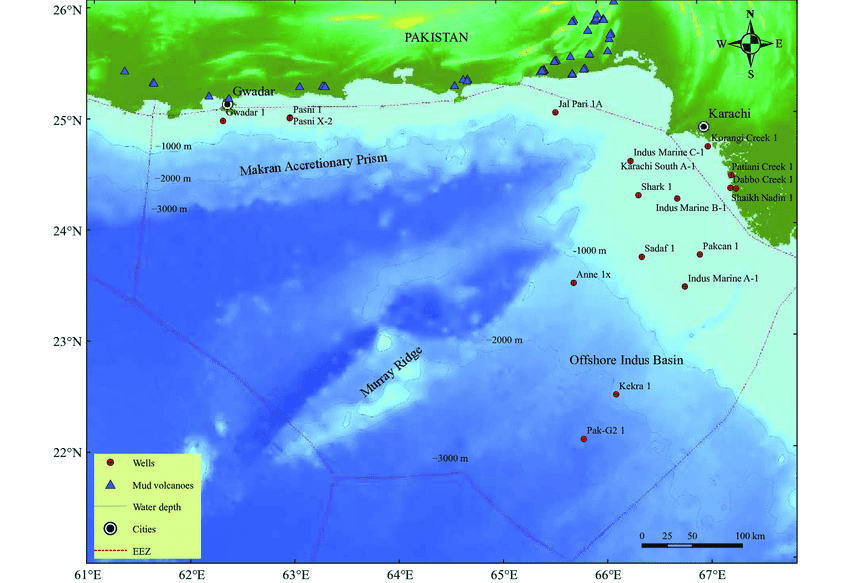

Pakistan’s Offshore Exploration: Challenges and History

- Early Attempts (1960s–1980s)

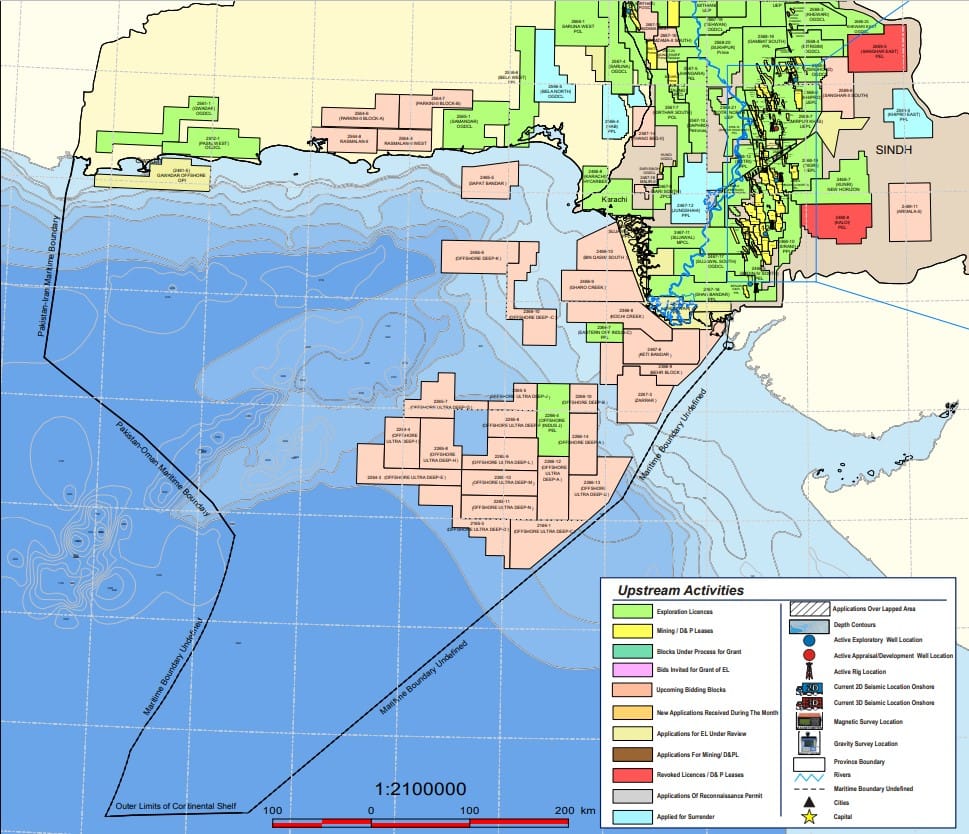

Pakistan’s offshore exploration began in 1963, with Sun Oil drilling three wells in the Indus Delta. Subsequent efforts in the 1970s and 1980s by Wintershall, Marathon, and OGDCL revealed limited success. Key findings included gas shows in the Miocene and shaly source rocks beneath the Deccan volcanics.

- Exploration Stagnation (1990s–2010s)

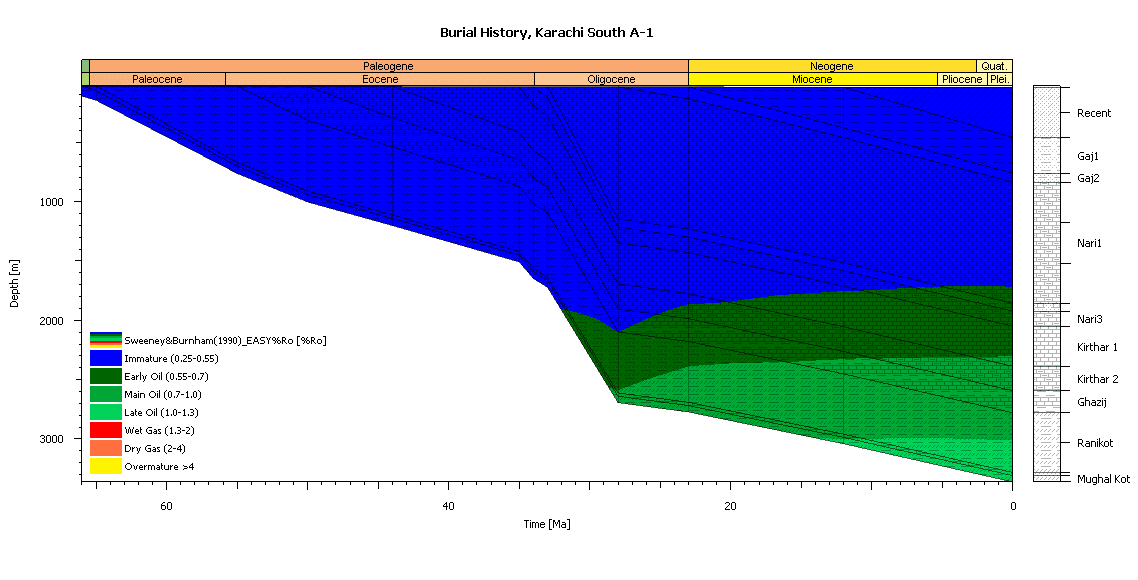

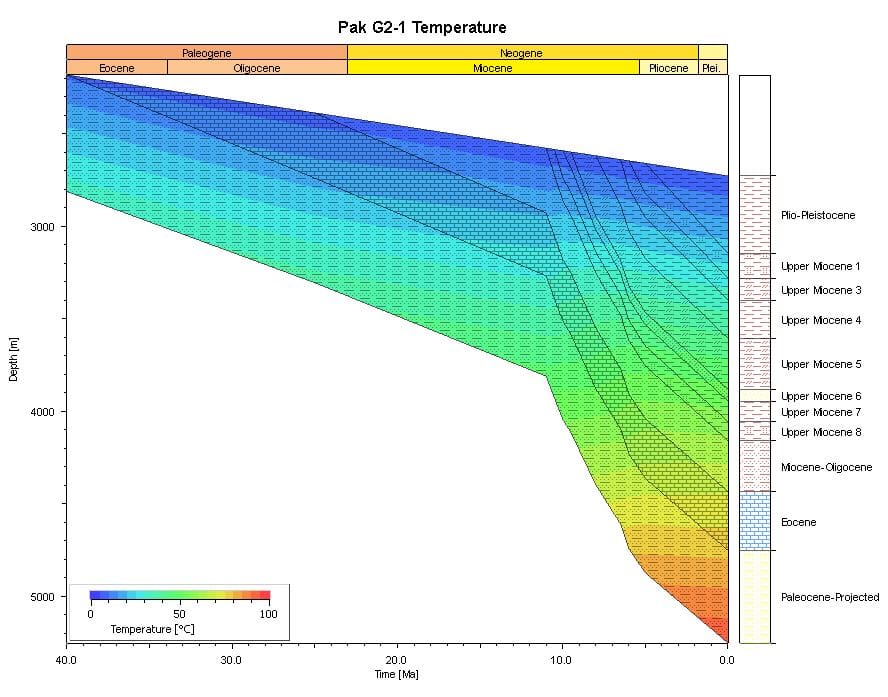

Despite the discovery of gas at Pakcan-1, efforts by international operators such as Total Energies, Oxy, and PPL yielded no major breakthroughs. The most recent well, Kekra-1 (2019), drilled by ENI, failed to confirm commercially viable resources.

- Current State

Pakistan’s offshore remains underexplored, with technical challenges, governance issues, and a lack of consistent policy direction deterring investment.

Lessons from Namibia for Pakistan

- Persistence and Long-Term Vision

Namibia’s success came after decades of effort and numerous dry wells. Pakistan must adopt a similar mindset, understanding that significant discoveries often require persistence over time. - Investor-Friendly Policies

Namibia’s transparent regulations and open licensing system encouraged international participation. Pakistan must revise its offshore policies to offer competitive fiscal terms, ensuring clarity and fairness for foreign investors. - Data-Driven Exploration

Namibia invested heavily in seismic data acquisition and geological modeling, reducing exploration risk. Pakistan should prioritize similar initiatives, including basin analog modeling and leveraging advanced seismic technologies. - Strategic Partnerships

Collaboration with supermajors like Shell and TotalEnergies brought cutting-edge technology and expertise to Namibia. Pakistan should foster partnerships with global leaders in offshore exploration. - Political and Economic Stability

A stable environment is crucial for attracting and retaining investors. Pakistan must focus on creating a favorable business climate, addressing governance issues, and ensuring policy continuity. - Technology and Innovation

Namibia’s adoption of advanced 2D and 3D seismic methods proved pivotal. Pakistan should invest in modern exploration technologies to improve success rates.

Conclusion: A Path Forward for Pakistan

Key steps include fostering an investor-friendly ecosystem, prioritizing data acquisition, and engaging with international experts. With sustained efforts and strategic planning, Pakistan’s offshore potential can transform into a vital resource for the nation’s energy needs.